SECTION 4.2: The Magic of Compounding

This work is licensed under an Open Educational Resource-Quality Master Source (OER-QMS) License.

![]()

One of the major themes of this little book is that your salary is not enough to make you comfortable and let you do all of the things you want to do. A major part of the strategy I recommend is putting your money to work for you. If you are at work making money while your money is at work making you money, then obviously you’ll be making a lot more money than if it was just you working. Money works for you when you invest it. Money isn’t doing a thing if you hide it under the mattress or leave it in a checking account. Money in a cookie jar is lazy money. It will not grow that way.

When I talk about putting your money to work I mean making itself grow. You can think of money as tomato seeds. If you plant those seeds in the right environment, they will grow an amazing amount, and keep doing so. Putting your money into a cookie jar is like planting seeds in the desert. Those seeds will never grow, but you can go back and dig them up later and plant them in fertile soil with plenty of water. As with seeds, money takes time to grow. For all of the “get rich quick” schemes out there (especially on the internet!), none of them work. You can’t get rich quickly. You have to get rich slowly and carefully. There are ways to make sure you get a bumper crop! Just as seeds need warmth, fertile soil, and plenty of water, money will only grow quickly under certain conditions.

To continue our tomato analogy, if you want a bumper crop of tomatoes, the best thing you can do is plant a lot of seeds. With investments, the more money you can invest early on, the quicker you will grow rich. If you could start with a $100,000 nest egg, you can be a millionaire in your early thirties. If you don’t invest the money and spend it on fleeting things, then you will end up like the countless athletes, musicians, and lottery winners that are now poor.

The big idea of compounding is this: You make interest on your money, usually determined yearly. Banks call this percentage an Annual Percentage Rate or APR. When you save, the bank pays you the APR on your money and it grows. The next year, you have your starting cash plus what you earned in interest, and the bank pays you the APR on that amount. The amount keeps growing and you keep earning interest in the growing balance—that’s compounding! It is critical to understand that when you borrow money, you pay the bank the APR. Note that word annual. That means you pay that amount of interest each and every year. In other words, the bank’s investment in you has them earning compounding interest, and it is coming out of your wallet! That’s why I take a general position that debt is bad.

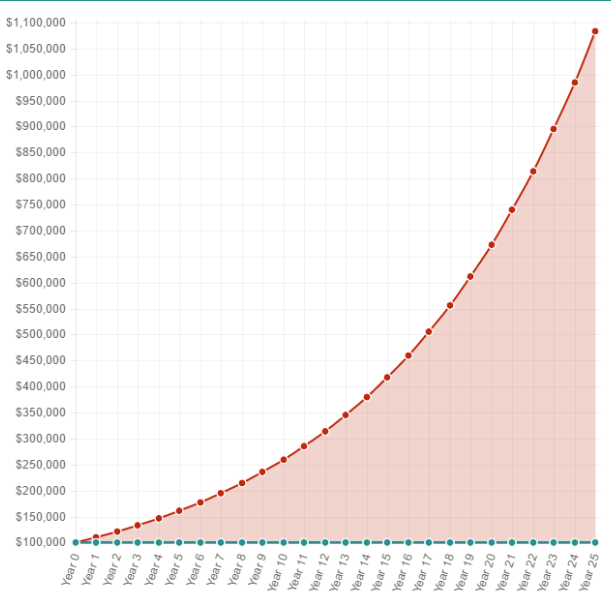

Figure 1: $100,000 over 25 years at 10% interest.

Note that the dots in Figure 1 do not form a straight line as they would if you were just stuffing money in a cookie jar every week and not earning interest. The dots in the graph above form a curve (sometimes referred to as a growth curve). That curve means that your money is growing faster and faster over time. The scenario in this graph would only work if you won the lottery or your long lost uncle died and left you a lot of money. My point in presenting it here was to demonstrate the power of compounding. Let’s look at a more likely scenario. Let’s say you open an online brokerage account with $2500 (most set this as the minimum). You decide to invest another $100 per month. Here is what you’ll end up with after 25 years:

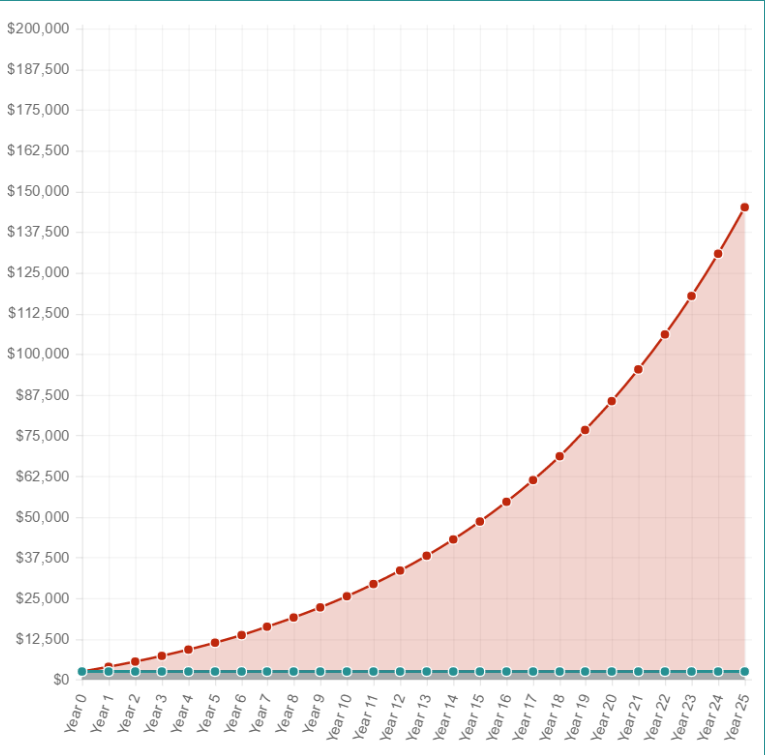

Figure 2: $2,500 + $100 / month for 25 years at 10%.

Note that the curve starts getting steeper much slower in Figure 2. This is because your money is building up slowly over time, and even the magic of compounding can’t do much in those early years when your portfolio is miniature. We can learn several lessons from this chart. The first is to start investing as soon as you can! Do not fall into the trap of convincing yourself that you’ll wait until later in life when you are making more money to start. Make investing a part of your budget right now. The second major lesson is that you can’t build up enough money to retire comfortably investing only $100 a month. It will grow impressively, but not it will not be as much as you need. I agree with the financial advisors on this one; you should invest as a percentage of your wages.

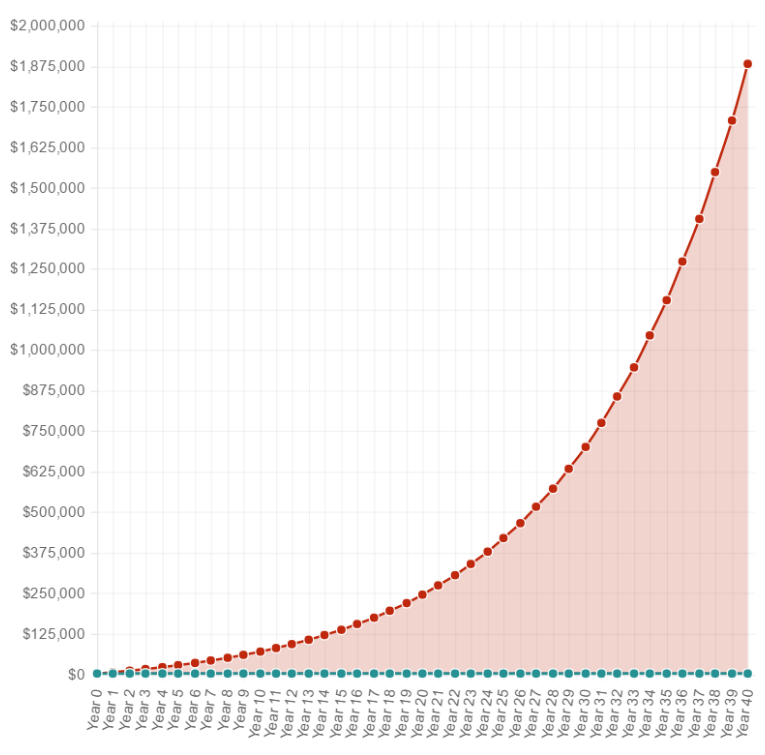

Let’s assume that you are more realistic about your retirement savings. You decide to follow my advice and save 10% of your income for retirement. Let’s further assume that you are making $40,000 per year (about right for a state job). Ten percent of $40K is $4K (multiply 40,000 by 0.10). Dividing that $4K by 12 months gives you a total monthly savings of $333. In that case, you get a chart like this:

Figure 3: 10% monthly on a $40,000 income over 40 years.

What are we supposed to learn from this chart? When you wisely invest 10% of your income for your entire career you will retire loaded. Given that your contributions will go up over time as your salary goes up (which the graph doesn’t take into account), you will be a multimillionaire!

References and Further Reading

The United States Securities Exchange Commission runs a really awesome website called Investor.gov. The site has a compounding interest calculator that I used to generate the charts in this section. You can find it at the following address:

[Back |Table of Contents | Next ]